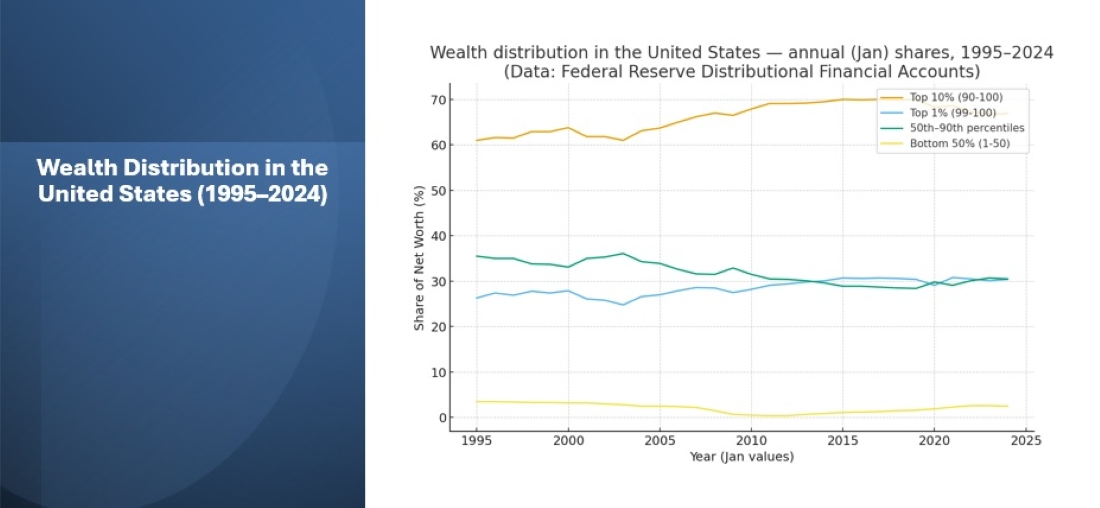

For all the talk about “equity,” America’s wealth gap has only grown wider — and government policy deserves much of the blame. According to data from the Federal Reserve’s Distributional Financial Accounts, the top 10% of households now control nearly 70% of the nation’s wealth, up from about 61% in 1995.

That trend didn’t happen by accident. It’s the direct result of decades of easy money, Washington spending, and a financial system that rewards speculation over savings. This widening wealth gap is not just an economic issue; it is a societal challenge that affects the fabric of our communities.

As policymakers introduced a series of interventions, the intended safety nets ended up strengthening financial hierarchies, resulting in most individuals experiencing stagnant or declining shares of the nation’s wealth. Despite the rollout of programs aimed at promoting fairness, the systems of credit expansion and focused relief primarily benefited those who already possessed assets, largely neglecting everyday workers. This has led to a consistent trend: each round of policies, while claiming to elevate the broader population, ultimately concentrates wealth among the affluent, emphasizing that structural decisions—not merely market dynamics—have deepened the economic divide.

Banks should be required to pay at least 4% interest on savings accounts to give 90% of Americans a fighting chance at clawing back some wealth. Only then can the middle class regain its footing and reclaim the role as the heart of the nation’s economic success.

Decades of Government Intervention, Same Results

This trend exacerbates the wealth gap, challenging the notion of the American Dream for many.

Understanding the Wealth Gap in America

Since the mid-1990s, the Federal Reserve and Congress have injected trillions into the economy — from stimulus checks to bank bailouts — each time promising to lift up working families. Instead, each new rescue inflated asset prices, making the rich richer and the middle class more dependent.

Top 1%: Up from 26% to over 30% of total wealth.

This pattern reinforces the wealth gap, emphasizing the need for systemic change.

Top 10% overall: Approaching 70% of all net worth.

Middle 40% (50th–90th percentiles): Down from 35% to about 30%.

Bottom 50%: Still clinging to just 2–3% of the nation’s wealth.

The financial crisis highlighted the disparities that contribute to the wealth gap.

The Cycle of Booms and Bailouts

Many families feel left behind, further widening the wealth gap.

Each economic era tells the same story — Wall Street gets the rescue, Main Street gets the bill.

The pandemic has exacerbated the wealth gap, with long-lasting implications.

1995–2002: Tech Boom and the First Warning

The decline of the middle class is directly tied to the growing wealth gap.

The dot-com crash wiped out small investors, but the big players bounced back thanks to cheap credit and the first modern bailouts.

2003–2009: Housing Bubble and Financial Crisis

Federal housing mandates, loose lending, and Fed manipulation of interest rates created a false sense of prosperity. When it burst, homeowners paid the price – and the banks were saved.

2010–2019: “Recovery” for Whom?

Low interest rates inflated markets, not paychecks. Asset owners saw record gains while wage earners fell behind.

2020–2024: Pandemic Stimulus and Inflation

Washington flooded the economy with trillions more in “relief,” driving up prices and further enriching those who already owned stocks, real estate, and businesses.

The Vanishing Middle Class

Only by addressing the wealth gap can we hope to achieve true economic equality.

The American middle class — once the engine of upward mobility — has seen its share of wealth erode. Rising costs, declining purchasing power, and tax policies that punish saving have squeezed families who play by the rules. Meanwhile, political elites call for more redistribution, as if the same government that distorted markets in the first place can fix the damage with more regulation and debt.

A Different Path Forward

If America wants to narrow the wealth gap, we don’t need more government intervention – we need less.

• End the era of perpetual stimulus and zero-interest manipulation.

• Restore sound money that rewards work and savings, not just leverage and speculation.

• Encourage small business ownership and investment, not dependency.

• Rein in the spending that fuels inflation and erodes middle-class wealth.

By empowering individuals to build lasting wealth through entrepreneurship and responsible stewardship, America can revive the promise of broad prosperity. Real reform begins with restoring trust in markets, letting people freely pursue opportunity, and shifting focus from top-down fixes to grassroots solutions. Banks should be required to pay at least 4% interest on savings accounts to give 90% of Americans a fighting chance at clawing back some wealth. Only then can the middle class regain its footing and reclaim the role as the heart of the nation’s economic success. Certainly the cost of such a mandate would show up in other banking products but it would be regulated in a way that protects the people it’s designed to help.

Beyond reforming banking practices, meaningful change also demands that policymakers prioritize fiscal responsibility and create an environment where honest work and prudent saving are rewarded, not penalized. By fostering genuine opportunities for entrepreneurship and ensuring that economic growth benefits those who build and innovate, America can chart a course back to broad-based prosperity. Only through these measures can the country restore faith in the promise of upward mobility and secure a future where the middle class thrives as the backbone of national strength and stability.