Before 1984, Social Security benefits were not subject to income tax. The Social Security Amendments of 1983 changed this by treating the benefits as taxable income. This legislation allowed for up to 50% of Social Security benefits to be taxable for individuals with income above certain thresholds.

Social Security was introduced as a form of social insurance to provide financial support for retirees, the unemployed, and other vulnerable groups. The Social Security Act of 1935 established this system, which is funded through payroll taxes on workers and employers.

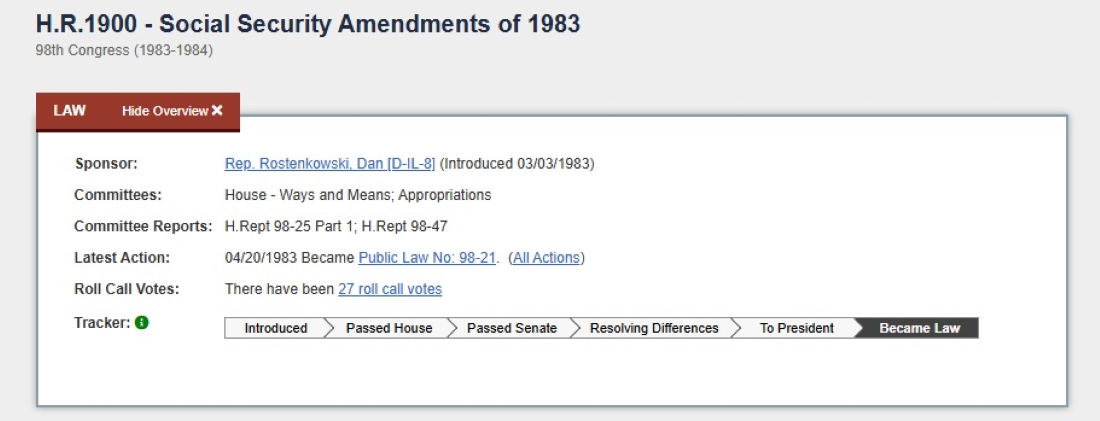

How did politicians sell the idea of taxing “social insurance” for retirees, the unemployed, and other vulnerable groups? Rep. Dan Rostenkowski [D-IL-8] introduced H.R. 1900 – Social Security Amendments of 1983 on March 3rd, 1983.

It’s Not Welfare. You Earned it.

The Social Security system is designed such that employees contribute 7.5% of every paycheck over the course of their working lives, typically spanning forty to fifty years. For an individual with an average annual income of $42,000, this equates to a total contribution of $157,500, which is matched by employers to reach a sum of $315,000. Despite these funds being pooled for other purposes, such as unemployment insurance, it highlights the substantial financial commitment made by American workers into the system during their careers.

A retiree who receives $21,000 annually from Social Security would need approximately fifteen years to recover their contributed amount, excluding any potential interest earned by the government on these funds. Consequently, an individual beginning to receive benefits at age 62 would be 77 years old before reclaiming their contributions, assuming no interest was accrued on the amounts collected by the government from the worker’s paychecks during their employment period.

Income Thresholds

For individuals, Social Security benefits may be taxed if your combined income exceeds $25,000, with up to 50% taxable between $25,000 and $34,000, and up to 85% taxable if over $34,000. For married couples filing jointly, the thresholds are $32,000 for no tax, up to 50% taxable between $32,000 and $44,000, and up to 85% taxable if over $44,000.

Loss of Trust in the Trust Fund

Once passed and signed into law by President Ronald Reagan, H.R. 1900 – The Social Security Amendments of 1983 became Public Law 98-21. “To ensure the solvency of Social Security Trust Funds…” is the way Public Law 98-21 begins. Social Security is often not referred to as a “trust fund,” but it functions as one.

The Social Security Trust Fund, or Old-Age and Survivors Insurance (OASI) Trust Fund, was created by the Social Security Act of 1935. It finances Social Security benefits for eligible recipients using payroll taxes, known as the Federal Insurance Contributions Act (FICA) taxes, paid by workers and employers.

A trust fund is a legal entity established to hold and manage assets for the benefit of specific individuals or organizations. In the context of Social Security, the Social Security Trust Fund operates similarly to other trust funds. It holds the payroll taxes collected from workers and employers, which are then used to finance benefits for eligible recipients. Despite its name, it functions more like a dedicated fund specifically for Social Security purposes.

How Much Money Has Been Borrowed from Social Security?

According to the Social Security Administration, a total of $2.9 trillion has been borrowed from the trust fund since 1965. This amount represents all the trust fund’s total assets, which currently stand at around $2.9 trillion.

Congress often raises taxes without adjusting income thresholds, increasing revenue but burdening lower-income taxpayers. For example, H.R. 1900 taxes up to 50% of benefits for individuals above certain income levels. Now, married couples with incomes over $44,000 may have 85% of their Social Security benefits taxed. In many parts of the United States, an annual income of $44,000 for a married couple is not a livable income.

If Congress cannot make Social Security payments tax-exempt again, it should raise the income thresholds for taxing benefits to $125,000 for individuals and $150,000 for married couples. If they really want to get it right, Congress needs to once again return Social Security benefits to a tax-exempt status. Over 90% of retirees in the United States receive monthly Social Security checks. Regardless of a retiree’s wealth, taxing this money is wrong in theory and practice.